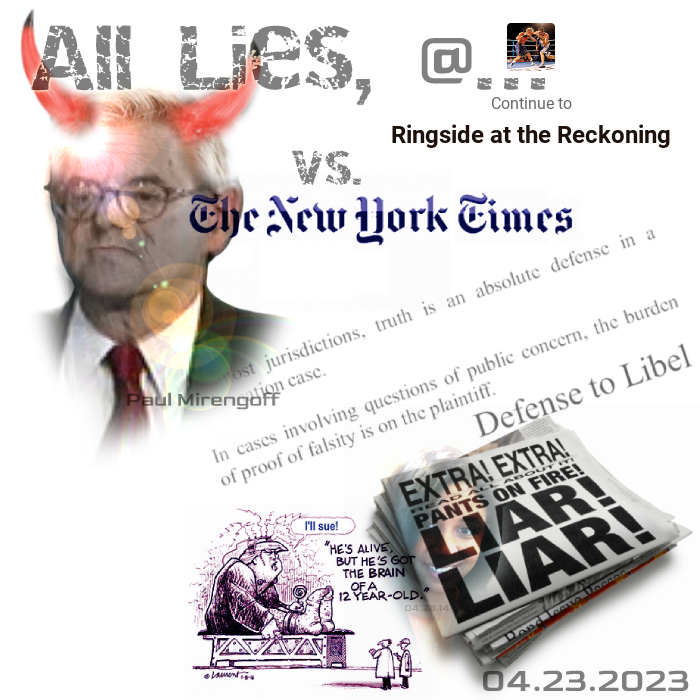

Each of them has gone after NY City Attorney Alvin Bragg, in posts overnight — into this morning. Paul Mirengoff’s is here…

Each of them has gone after NY City Attorney Alvin Bragg, in posts overnight — into this morning. Paul Mirengoff’s is here…

And John Hinderaker’s libel is here.

Each of them claims that lying about why Stormy Daniels was paid by Michael Cohen… is no crime. That is false — the grand jury indictment proves it. And each of the boys knows it. Each of them argued for the criminal and impeachment-conviction of Bill Clinton, for lying about Monica Lewinsky, as felonies. [Links to those tens of dozens of posts available on request.]

But they each NOW claim that Tangerine’s lies, then memorialized as legal fees, and documented by checks, and treated not as campaign expenditures, but as regular Trump Org. business expenses… cannot be elevated to felonies, under New York law. About this, they both know full well… they are lying.

But they each NOW claim that Tangerine’s lies, then memorialized as legal fees, and documented by checks, and treated not as campaign expenditures, but as regular Trump Org. business expenses… cannot be elevated to felonies, under New York law. About this, they both know full well… they are lying.

While it is true that the Bragg prosecution is one of Tangerine’s smaller exposures to felony jail time — as Paul openly now admits, the top secret documents case is almost iron-clad, in proof of multiple national security felonies… one way or another, he is going to be found guilty of important felonies against the people of this nation.

Even so, it may take a minute to go to trial, with USDC Judge Aileen Cannon (a Trump appointee) slow walking it. But Trump will be found guilty of felonies on some or all of the 90-ish felony counts he now faces — in four courtrooms around the Eastern seaboard.

In any event — saying that willful, knowing, financial lies — in business records, are not felonies… is just silly (and contradicts their numerous claims about Bill Clinton, where no payments were ever even alleged, by the way).

Yep — people go to jail all the time for lies on their business taxes, and state corporate filings (ones with knowing, intentional lies in them). It happens that NY AG Leticia James only charged his $450 million of loan-, and tax-frauds, civilly — so as to get a recovery sooner, for the people of New York. That was smart advocacy — under-charging the offense to get a dead bang win.

Yep — people go to jail all the time for lies on their business taxes, and state corporate filings (ones with knowing, intentional lies in them). It happens that NY AG Leticia James only charged his $450 million of loan-, and tax-frauds, civilly — so as to get a recovery sooner, for the people of New York. That was smart advocacy — under-charging the offense to get a dead bang win.

But make no mistake: those too were felonies, as a matter of law.

So do shut your yaps, John and Paul.

Out.

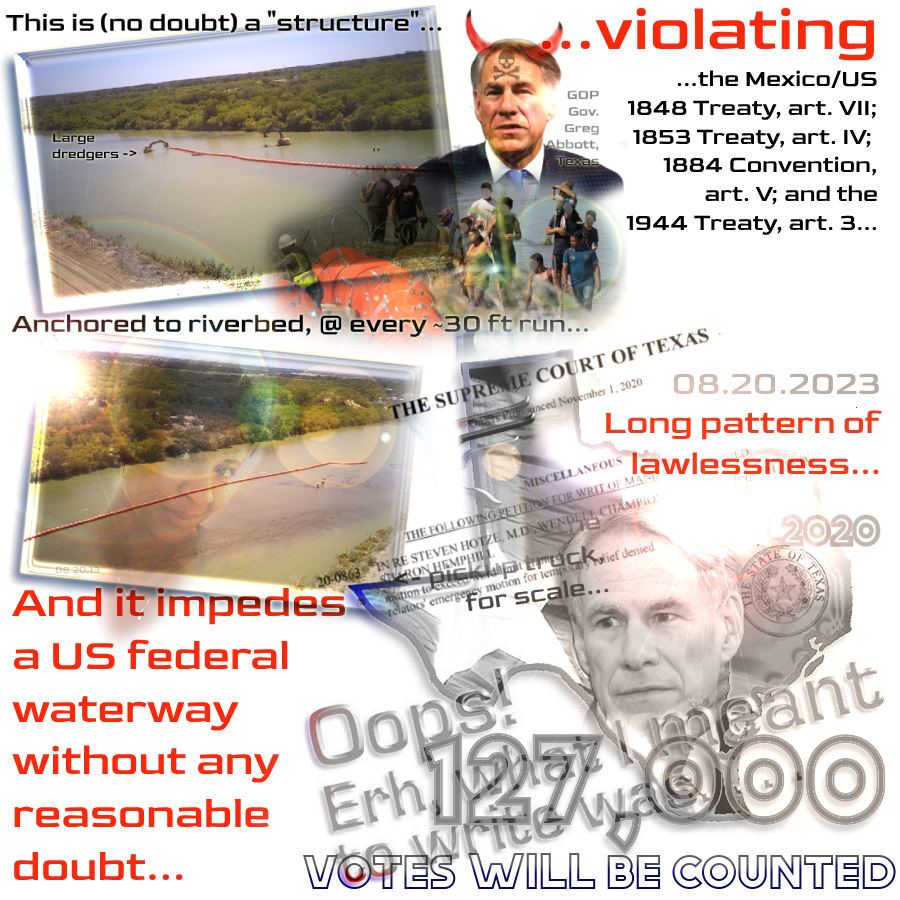

This is a small update — as Judge Ezra has also ruled that all of the federal government Rivers and Harbors Act claims, and the immigration laws which vest singular authority at the federal level for border matters… remain intact.

This is a small update — as Judge Ezra has also ruled that all of the federal government Rivers and Harbors Act claims, and the immigration laws which vest singular authority at the federal level for border matters… remain intact.